How Can You Build an Emergency Fund When Prices Are High?

Start small. Even saving $10 or $25 per paycheck moves you in the right direction. Open a separate, FDIC-insured high-yield savings account and automate your contributions. Cut one or two non-essential expenses to free up cash. When groceries, rent, and utilities take most of your income, the goal is not perfection; it is progress. One month of expenses saved is a meaningful starting point before working toward three to six months.

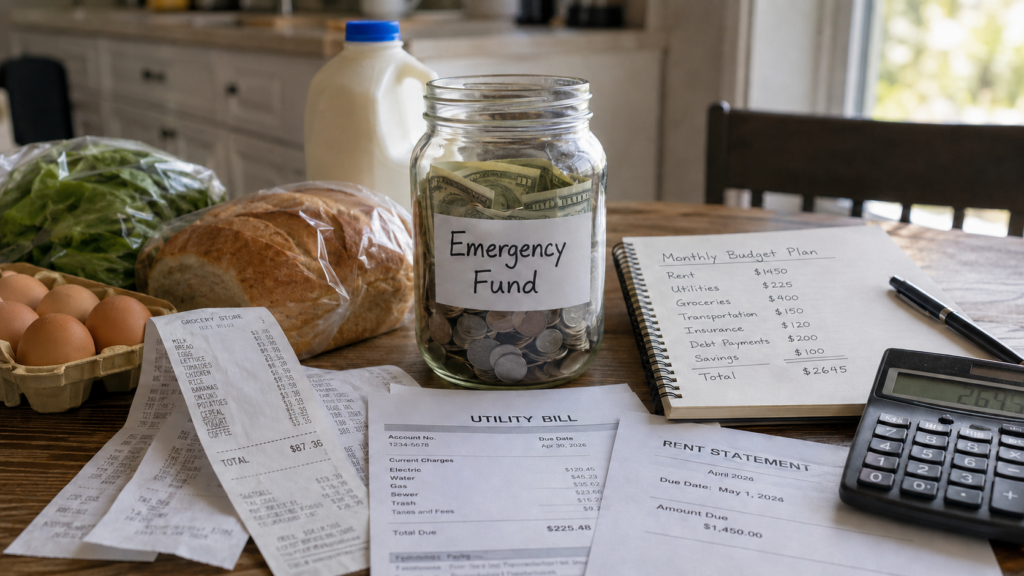

Why an Emergency Fund Matters More When Prices Are High

When the cost of living rises, the gap between income and expenses shrinks. That gap is where emergency savings live.

A job loss, a car repair, a medical bill, or a broken appliance can send a household into financial crisis when there is no cushion in place. Without savings, most people turn to credit cards, personal loans, or borrowed money from family. That often means high-interest debt that takes months or years to pay off.

Consumer finance data consistently shows that a large share of American households are living paycheck to paycheck. When an unexpected expense hits, the options narrow quickly. An emergency fund is the tool that keeps a bad situation from becoming a much worse one.

With grocery prices, rent, utilities, insurance, and gas all running higher than they did a few years ago, the pressure on household budgets is real. That pressure makes building emergency savings harder, but it also makes having them more important.

What Is an Emergency Fund?

An emergency fund is money set aside specifically to cover unexpected expenses or a sudden loss of income. It is not a vacation fund, a down payment account, or money earmarked for holiday shopping. It exists for one purpose: financial protection when something goes wrong.

Common legitimate emergencies that warrant using this fund include:

- Unexpected medical bills or a trip to the emergency room

- Car repair or sudden vehicle breakdown

- Job loss or a significant cut in work hours

- Major home repair such as a water heater failure or roof damage

- A sudden funeral or family crisis requiring travel

An emergency fund is not for sales, impulse purchases, or discretionary spending. Keeping it defined this way is important. The fund only works if it stays intact until a real emergency arrives.

How Much Should You Save in an Emergency Fund?

The widely cited guideline from financial planners is three to six months of essential living expenses. That means rent or mortgage, utilities, groceries, transportation, minimum debt payments, and any non-negotiable bills.

For a household spending $3,000 per month on essentials, a three-month fund would be $9,000. A six-month fund would be $18,000.

Those numbers feel overwhelming to many people, especially those already dealing with high prices and tight budgets. That is completely understandable.

A more practical starting target for most people is one month of essential expenses. One month provides meaningful protection against a small unexpected bill without feeling impossible to reach. Once that milestone is hit, extending toward three months becomes the next goal.

Some personal finance educators refer to a smaller initial target as a “starter emergency fund.” Dave Ramsey popularized a $1,000 starter fund as a first step before paying down debt. Others suggest one month of expenses. The exact number is less important than starting and being consistent.

The key insight: any amount saved is better than zero. A $500 cushion can prevent a $500 car repair from landing on a high-interest credit card.

Where to Keep Your Emergency Fund

Your emergency fund should be:

- Liquid: you need to be able to access it quickly, without penalties

- Safe: it should not be subject to market losses

- Separate: Keeping it away from your checking account reduces the temptation to spend it

The best options for most people are:

High-yield savings account (HYSA): These accounts, offered by online banks and some credit unions, pay significantly more interest than a traditional savings account. They are FDIC-insured up to $250,000 per depositor, per institution. In a high-interest-rate environment, a HYSA can earn a meaningful return while your money stays accessible. This is the most commonly recommended option for emergency funds.

Traditional savings account at a bank or credit union: Lower interest rates than HYSAs, but still FDIC- or NCUA-insured and accessible. Better than keeping the money in your checking account.

Money market account: Similar to a high-yield savings account in terms of FDIC insurance and liquidity. Often comes with a debit card or check-writing ability, which can be useful in emergencies.

What you should avoid for emergency savings: stocks, mutual funds, cryptocurrency, or any investment that can lose value quickly. Emergency funds are not investment accounts. If the market drops 30 percent the week your car breaks down, you cannot afford to wait for a recovery.

How High Prices Change the Emergency Fund Strategy

Inflation and rising consumer prices affect emergency savings in two important ways.

First, the target amount goes up. If groceries, rent, and utilities are more expensive than they were two or three years ago, then three months of essential expenses today costs more than it used to. That means households need a larger dollar amount in savings to cover the same period of time.

Second, there is less money left over to save. When a larger share of each paycheck goes toward food, housing, transportation, and energy, there is simply less remaining. Building savings becomes slower.

This does not mean giving up on an emergency fund. It means adjusting the strategy.

Step-by-Step: How to Build an Emergency Fund on a Tight Budget

Step 1: Calculate Your Actual Monthly Essentials

Write down every non-negotiable monthly expense. This includes rent or mortgage, electricity, water, gas, groceries, transportation costs, minimum debt payments, and any essential insurance premiums. Total these up. That number is your monthly essential spending and your emergency fund target baseline.

Step 2: Open a Separate Savings Account

Do not keep your emergency fund in your checking account. Open a dedicated savings account, ideally a high-yield savings account with an online bank. Keeping the money separate reduces the urge to spend it and makes it psychologically easier to leave it alone.

Step 3: Set a Small, Realistic Weekly or Monthly Contribution

If you can only save $20 per week, save $20 per week. Over a year, that becomes more than $1,000. If your budget allows $100 per month, that becomes $1,200 in 12 months. Consistency matters far more than the size of each contribution.

Automate the transfer if possible. Many banks allow you to set up an automatic transfer on payday. When the money moves before you see it, you are less likely to spend it.

Step 4: Audit Your Spending for One Month

Review your bank statements and credit card statements from the past 30 days. Identify subscriptions, memberships, or recurring charges that you do not regularly use. Many households find $30 to $80 per month in unused or forgotten subscriptions. Canceling even two or three can meaningfully increase savings capacity.

Step 5: Redirect Windfalls to Your Emergency Fund

Tax refunds, bonuses, overtime pay, birthday money, and side income can accelerate emergency savings dramatically. Rather than spending a windfall, commit to putting at least half of it directly into your emergency fund. One tax refund alone can fund a starter emergency fund for many households.

Step 6: Use the 24-Hour Rule for Non-Essential Purchases

For any non-essential purchase over a set threshold (many personal finance experts suggest $50 or $100), wait 24 hours before buying. This pause reduces impulse spending and frees up money for savings. It is a simple habit that adds up over months.

Step 7: Reassess Every Three Months

Your income, expenses, and cost of living will change. Every three months, revisit your emergency fund progress. Increase your contribution amount when possible, especially after a raise, a paid-off debt, or a reduction in a monthly bill.

Emergency Fund vs. Credit Card Debt: Which Comes First?

This is one of the most common personal finance questions, and there is no single right answer. It depends on your interest rates, income stability, and personal situation.

The general guidance from most consumer finance experts and organizations such as the Consumer Financial Protection Bureau (CFPB) is to do both at the same time, at least in the early stages.

Here is why: if you put every available dollar toward debt and a $700 car repair hits, you will likely charge it on a credit card, adding back the debt you just paid down. The cycle continues.

A common approach is to build a small starter emergency fund (between $500 and $1,000), then aggressively pay down high-interest credit card debt, then build the full three-to-six-month fund.

Waiting until all debt is paid before saving anything means living with zero financial buffer for months or years, which is a risky position.

How to Save for Emergencies on Irregular Income

Freelancers, gig workers, seasonal employees, and anyone with variable income face a different challenge. When your paycheck is not the same every month, fixed savings targets are harder to hit.

Two strategies that work for irregular income:

Percentage-based saving: Instead of saving a fixed dollar amount, commit to saving a fixed percentage of every payment you receive, 10 percent, 15 percent, or whatever your budget allows. When income is higher, you save more. When income is lower, you save less, but still save something.

High-income month banking: In months when income is unusually high, resist the urge to spend freely. Instead, save aggressively in those months to compensate for the slower ones. Treat a strong income month as an opportunity to build a bigger buffer.

Irregular income households may also need a slightly larger emergency fund target since income disruptions can be harder to predict.

Emergency Fund Progress Tracker

| Milestone | Approximate Value | What It Covers |

| Starter Fund | $500 to $1,000 | Minor car repair, small medical bill |

| One Month Essentials | Varies by household | One month of rent, food, utilities, transport |

| Three Month Fund | 3x monthly essentials | Job loss of up to 3 months, major emergency |

| Six-Month Fund | 6x monthly essentials | Extended job loss, serious illness, or major repair |

Emergency Fund Checklist

Use this checklist to track your progress:

- I know my monthly essential expenses total

- I have opened a separate savings account for emergencies

- I have set up an automatic transfer on payday

- I have reviewed subscriptions and canceled unused ones

- I have committed a percentage of any windfall to my emergency fund

- I have defined what counts as a real emergency

- I am not touching this fund for non-emergencies

- I review my progress every three months

Key Takeaways

- An emergency fund is savings set aside only for unexpected expenses or income loss.

- The traditional target is three to six months of essential living expenses, but one month is a strong starting point.

- High prices increase both the target amount you need and the difficulty of saving, but make an emergency fund more important than ever.

- Keep your emergency fund in a separate, FDIC-insured high-yield savings account.

- Automate contributions, audit spending, and redirect windfalls to build savings faster.

- Building a small starter fund while paying down debt is better than waiting until all debt is eliminated.

- Irregular income earners should use percentage-based saving and bank their high-income months.

Frequently Asked Questions

Q1. How much should I have in an emergency fund?

Most personal finance guidance recommends three to six months of essential living expenses. If that feels out of reach, start with a goal of $500 to $1,000, then build toward one month, and eventually three months. Your target should reflect your own income stability, household size, and expenses.

Q2. Should I save for emergencies or pay off credit card debt first?

Ideally, do both. Build a small starter emergency fund first, then split available money between debt payoff and emergency savings. Going all-in on debt with no savings leaves you financially exposed to the next unexpected expense.

Q3. Can I invest my emergency fund in stocks or cryptocurrency?

No. Emergency funds should not be placed in investments that can lose value. The money needs to be safe, liquid, and accessible immediately. A high-yield savings account or money market account is the right vehicle.

Q4. What if I can only save $10 or $20 a week?

Start there. Ten dollars per week becomes $520 in a year. Twenty dollars per week becomes $1,040. The habit of saving matters as much as the amount, especially in the beginning. Increase contributions as your budget allows.

Q5. How do I stop myself from spending my emergency fund?

Keep it in a separate account from your checking account, preferably at a different bank or institution. The slight friction of transferring money reduces impulse access. Define clearly what counts as an emergency before you are in one.

Q6. Does inflation affect how much I need in an emergency fund?

Yes. If your monthly expenses are higher due to rising prices, your emergency fund target should reflect your current cost of living, not what you spent two or three years ago. Revisit your target number annually.